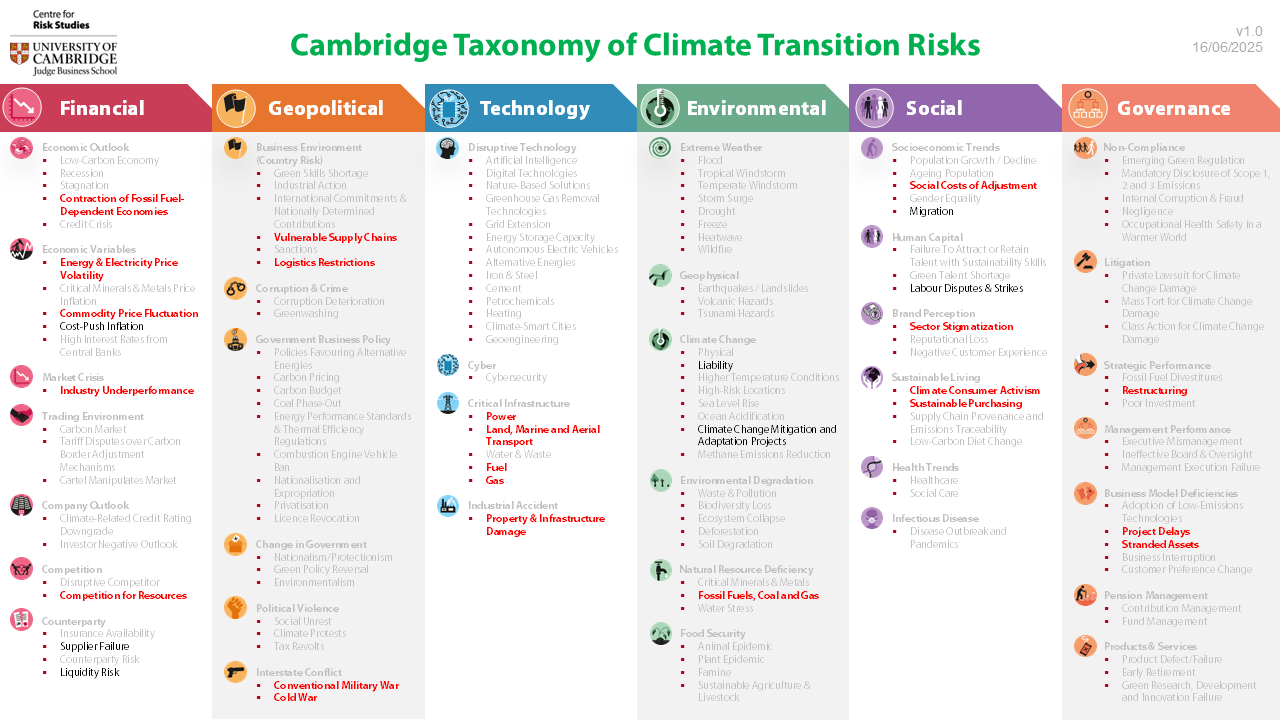

The closure of the Strait of Hormuz has disrupted a major share of global oil and liquefied natural gas (LNG) supply, exposing how vulnerable the world’s energy system – and climate‑transition planning – remains to geopolitical chokepoints. The event illustrates how a single disruption can trigger systemic transition risks, as mapped in the Cambridge Taxonomy of Climate Transition Risks:

- Financial: Energy, electricity and commodity price fluctuation; resource competition; industry underperformance; and inflation

- Geopolitical: Vulnerable supply chains, logistics restrictions, conventional military conflict and cold-war proxy

- Technology: Power; fuel; gas; land, marine and aerial transport; and property & infrastructure damage

- Environmental: Fossil fuels and gas deficiency

- Social: Social costs of adjustment, sectorial stigmatization and demand for alternative options

- Governance: Stranded assets, project delays and organisational / country-level restructuring

Closure of the Strait of Hormuz

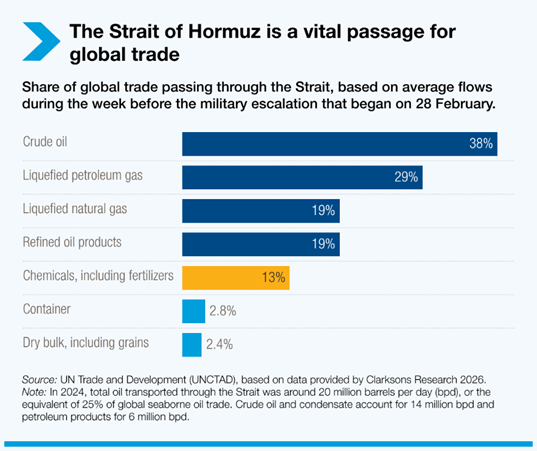

The Strait of Hormuz is one of the world’s most strategically important maritime corridors, linking the Persian Gulf to the Gulf of Oman. Roughly one‑quarter of global seaborne oil trade and nearly one‑fifth of liquefied natural gas (LNG) flows pass through this narrow channel. While Saudi Arabia and the United Arab Emirates can divert limited volumes through pipelines, most Gulf producers – including Iraq, Kuwait, Qatar, Bahrain and Iran – depend overwhelmingly on this route. Asian importers such as Japan, South Korea, China and India are similarly exposed.

The sudden halt in tanker movement demonstrates how quickly geopolitical tensions can destabilise fuel supply chains, raising the urgency of integrating transition‑risk thinking into energy security planning.

Climate transition risks

The Cambridge Taxonomy of Climate Transition Risks offers a structured view of how climate transition risks propagate across interconnected systems. Applied to the Hormuz closure, it highlights both immediate and emergent risks across six systemic risk classes.

Financial

- Energy & Electricity Price Volatility: Supply chain disruptions have triggered steep rises in crude oil, gasoline and LNG prices, with Brent crude topping $100–126 per barrel and Asian LNG spot prices doubling.

- Recessionary Pressures in Fossil-Fuel–Dependent Economies: Energy shortages have strained economies reliant on imported fuel. Several countries have reported production cuts, forced austerity measures and temporary closures, including school shutdowns in Pakistan and Laos to manage fuel scarcity.

- Competition for Resources: With 20% of global oil supply temporarily removed from the market – 80% of it destined for Asia – major Asian buyers are competing aggressively for alternative crude and LNG.

- Commodity Price Fluctuation & Industry Underperformance: Energy‑intensive sectors (including refining, petrochemicals, metals, fertilizers and manufacturing) face rising costs and narrowing margins due to fuel shortages and higher shipping and insurance prices: Knock‑on effects on commodity markets resulting from the loss of roughly one‑third of global helium and fertilizer supplies include heightened risks to semiconductor manufacturing and the potential for future food shortages.

- Emerging risks: Cost-Push Inflation, Supplier Failure and Liquidity Risk are beginning to spread as companies absorb rerouting, delays and insurance‑premium surges.

Geopolitical

- Vulnerable Supply Chains: Near‑zero maritime traffic has prompted rerouting, port congestion and significant delays. Disruptions extend beyond energy to food, medicine, electronics and other consumer goods due to longer routes and higher insurance costs.

- Logistics Restrictions: Carrier withdrawals, tanker queues, permission‑based vessel movement and widespread rerouting have reshaped global shipping patterns almost overnight.

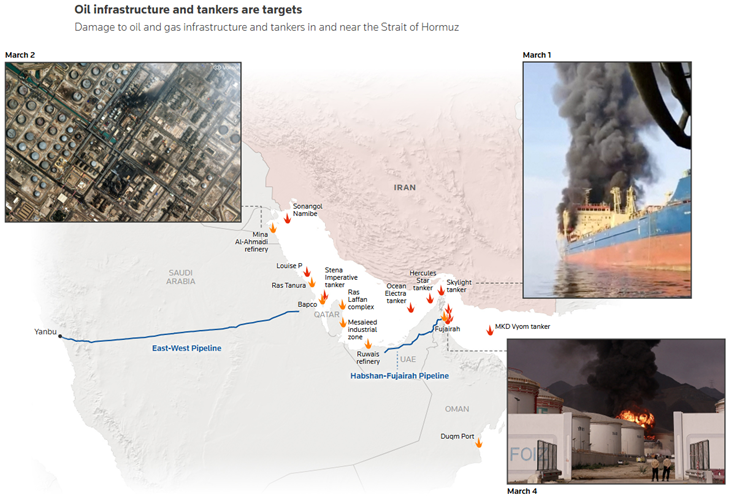

- Conventional Military Conflict: The closure occurs amid active strikes between the U.S., Israel and Iran, with retaliatory missile and drone attacks raising the risk of escalation.

- Cold‑War Proxy: Iran‑aligned groups have threatened other strategic routes, including Bab al‑Mandeb, risking further disruption and widened geopolitical fragmentation.

Technology

- Power Systems: Rising oil and gas prices threaten the energy inputs critical for data centres, telecom networks and industrial automation, especially in gas‑dependent Asian economies already shifting to coal or nuclear to maintain power supply.

- Land, Marine and Aerial Transport: Tanker traffic has collapsed by 95%, forcing shipping companies to suspend operations. Aviation has been affected by fuel shortages, high insurance premiums and reduced traffic in risk zones.

- Fuel (Oil): Sharp reductions in global oil supply are pushing producers to curtail output while consuming nations release strategic reserves. Simultaneous disruption to oil and LNG magnifies systemic risk.

- Gas (LNG): Around 20% of global LNG exports are affected. Qatar halted LNG production after facility attacks, and European gas prices doubled within days.

- Property & Infrastructure Damage: More than 21 attacks on ships and maritime infrastructure have been recorded, alongside strikes on industrial assets across the region.

Environmental

- Fossil Fuels & Gas: Hundreds of tankers initially anchored outside the Gulf to avoid risk before traffic waned to near zero, creating immediate supply deficits.

- Emerging: Producer shut‑ins and infrastructure damage raise Liability Risks for energy companies. Emergency measures – such as Japan releasing reserve oil – may temporarily deprioritize Climate Change Mitigation & Adaptation Projects, but could also accelerate diversification toward renewables.

Social

- Social Costs of Adjustment: Energy price spikes have increased transport, food and household costs, disproportionately affecting low‑income populations. Humanitarian operations face delays of up to six months due to higher fuel and shipping prices.

- Sector Stigmatization: The crisis intensifies scrutiny of fossil‑fuel reliance and highlights the vulnerabilities of global oil dependence.

- Climate Consumer Activism & Sustainable Purchasing: High fossil‑fuel prices historically heighten public interest in renewables. The current shock is prompting renewed debate on positioning renewables as “energy security tools”.

- Emerging: Cost‑of‑living pressures, instability and energy shortages may drive Labour Disputes or Migration flows if prolonged.

Governance

- Stranded Assets & Project Delays: Forced shutdowns and storage constraints have created temporary stranded assets. Several Gulf producers curtailed operations once storage filled and exports halted.

- Restructuring: Refineries worldwide have reduced runs or shut units due to limited crude, while QatarEnergy halted gas liquefaction in an operational restructuring of production.

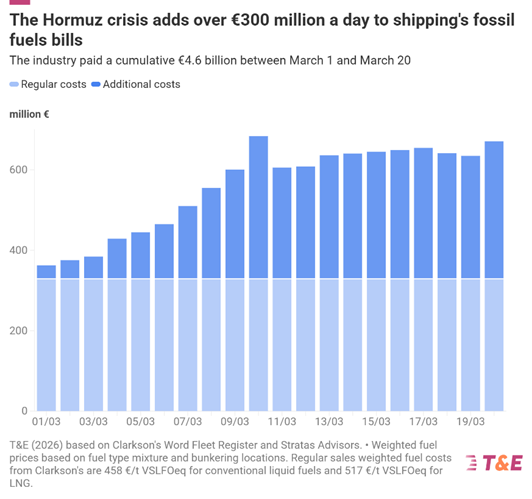

Case study: The Maritime shipping industry

The closure has imposed acute strain on shipping, with estimated industry losses of €340 million per day. Rerouting around chokepoints, congestion and heightened insurance demands underscore the sector’s vulnerability to oil and gas price volatility. Regions less dependent on fossil fuels show greater resilience, strengthening the argument for accelerating electrification, e‑fuels and efficiency improvements to reduce systemic exposure to geopolitical supply shocks.

Conclusions

The Hormuz closure demonstrates how geopolitical disruption can cascade through global financial systems, supply chains, energy infrastructure and social stability. Dependence on fossil‑fuel chokepoints deepens vulnerabilities during a disorderly transition. Strengthening preparedness, diversifying energy systems and adopting systemic‑risk frameworks are essential for a more resilient low‑carbon future. The Cambridge Centre for Risk Studies continues to support organisations in navigating these evolving risks.

Contributed by María Fernanda Lammoglia Cobo

Leave a Reply